As analysed in our previous release reviewing the USS pension adjustment, the University of Birmingham’s annual accounts for 2018/19 (pdf) present a rather misleading and questionable £115.4m bottom line deficit. This report summarises the underlying performance and highlights the key take aways from this year’s financials; in particular, what we now know about income, debt, staff costs, and senior management remuneration.

Deficit driven by discredited 2017 pension scheme valuation

The overall deficit was driven by the highly judgmental pension adjustment of £126.7m, which, the University argues, reflects their share of the USS deficit under the flawed and widely discredited 2017 valuation. This was a one-off ‘unrealised’ loss and the University has acknowledged that £81.6m would immediately reverse out next year. This leaves an underlying surplus of £11.3m (on a like for like basis with the prior year £15.4m surplus) or a £33.8m deficit if we account for the revised 2018 valuation of the USS scheme. In either case this leaves the University in a reasonably strong financial position overall compared to other institutions across the sector, although, as we will see, with increased levels of risk due to a high fixed cost base and increasing reliance on international student fees.

Income and debt position: increasing reliance on overseas income and debt finance

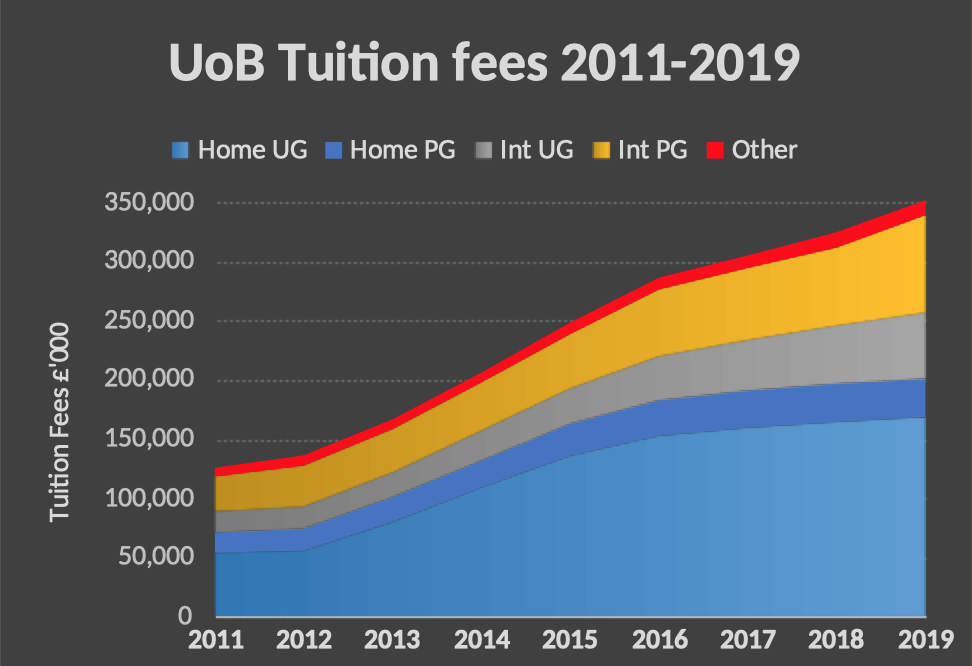

While staff salaries flat lined and once again fell behind inflation due to the derisory 2% 2018/19 pay offer, the University saw another major leap in international tuition fee income driven by high course fees and increasing international student numbers. This was on the back of previous hikes in home student fees since 2011 and the removal of the student number controls in 2015. Tuition fees now represent 49.1% of total University income (£351.8m), while international tuition fees have risen to 19.3% of total income (£138.1m):

One case example illustrates the inequity between these cumulative fee increases and the miserly pay offers in recent years. In 2019/20 an international student on an MSc post graduate taught programme might pay up to £24,000 per year in fees so that a large lecture to 300 students can generate as much as £20,000 per contact hour in fee income [1], while a grade 7 Teaching Fellow will earn just £18.75 (up 33p on 2018/19 pending outcome of current UCU dispute) per contact hour in gross salary including holiday pay. Such a module will need many seminars and office hours, plus preparation time, but modelling this under the latest University workload models would still leave a total staff cost per week of just £900 to £1,300 against three contact hours worth fees of £60,000, depending on whether all lectures and classes are delivered by a lecturer or Teaching Fellow or both [2]. This gives a marginal profit of as much as 4500% to 6500% per student for some of our large internationalised MSc courses, strongly incentivising the University to increase student numbers and module sizes.

But instead of investing these huge fees into secure, well paid and well trained jobs, an analysis of the University’s expenditure in recent years shows they have invested in physical assets, which now generate an annual depreciation charge of £65.7m, senior faculty pay, and the front loaded £100m cost of the new campus in Dubai, while casualising the workforce, cutting pay against inflation, and further milking our international students like cash cows.

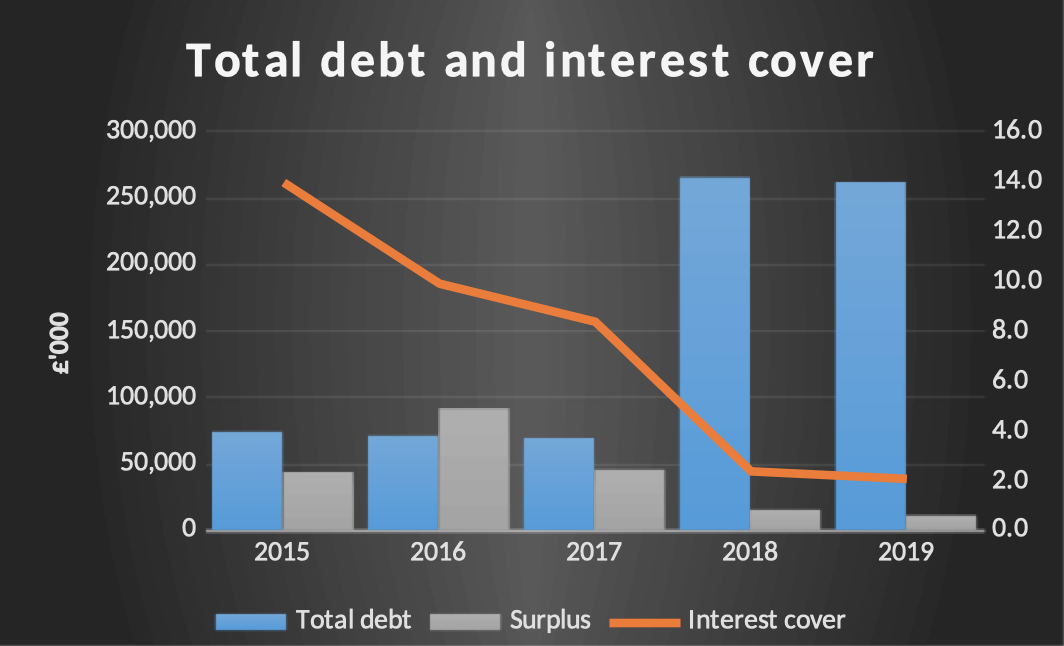

Despite the drop in the core surplus to £11.3m in 2018/19 (excluding pension adjustments) operating cash surplus has grown once again to a record £77.7m. This removes all one-off adjustments and estimates in the accounts and shows that the University is still a cash rich institution based on core operating activities. For the second year in a row, however, the large core surplus has been more than spent on fixed assets, with investment coming to £164.0m for 2018/19 (and £195.9m in 2017/18). The difference funded largely by debt.

As tuition fees have replaced the core government grant since 2010, the University’s surplus is therefore increasingly exposed to variable returns, particularly on the international market, while their debt and physical estates grow to leave them with a mounting fixed cost base. Per note 8. and note 16., £200m of unsecured loans taken out in the previous financial year now leave the University with annual interest payments of more than £10m per year and an interest cover (operating surplus over interest expense) of just 2.1 times (2.4 times in 2017/18).

In negotiations, University management will refer to uncertainty in future UK tuition fees and REF outcomes when asked about poverty pay, casualisation, subsidised childcare, and so on, however the reality is that they have introduced a ‘business model’ that is now reliant on high fees, debt, and cheap insecure labour. This leaves those on such casual contracts as directly bearing the risk of projects like the new Dubai campus and any future shocks to international student recruitment.

Staff costs: one rule for those at the top, another for everyone else

As previously reported by BUCU, the disparity in pay offers for those at the top of the institution and those across the pay grades has been a theme at UoB for many years. The 2018/19 accounts show an overall salaries cost of £309m up from £276m last year so that staff costs continues to be the single largest expense and has increased slightly as a proportion of overall income on the previous year. Average pay at the University, excluding the Vice Chancellor, increased to £40,881 (up 6.3% from £38,463), however this drops to £38,752 (up 4.4%) when one excludes the staff the University employs on more than £100,000 pa. The remaining 4.4% increase reflects in part the below inflation pay offer for 2018/19 of 2%, together with an increase in the proportion of academic and professional staff (up 5.4%) over lower paid technical and clerical posts (up just 1%), together with automatic increments for existing staff. This somewhat halts the trend in recent years in which average pay at UoB has flat lined or even fallen due to increasing casualisation and high staff turnover, but is consistent with yet another like for like pay cut in real terms due to the 2018/19 pay offer.

At the very top of the pay scales, UoB significantly increased the number of staff earning over £100,000 pa. to 170 (from 108 last year), the biggest increase we have ever seen in this category. Further analysis of this figure shows that this was almost entirely due to new posts, either through recruitment or promotion. These new posts required a total investment of approximately £8.9m [3]. This can be compared directly with the pay increase won by UNISON after 6 days of strike action, the first above inflation pay rise at UoB for more than 10 years, winning a graduated offer of 4.85% (band 200) to 3% (bands 400 and 500). This affects approximately 2,100 (FTE) staff from 1 August 2019 and will lead to an overall pay rise for low paid staff of approximately £0.6m over and above the University’s initial offer, so that an additional £1.6m pa will be invested in staff pay through 2019/20 [4]. This means that the University has invested approximately 5.5 times more in just 62 individuals in 2018/19 than they were prepared to invest in the entire administrative and support workforce of 2,100 full time equivalent posts in 2019/20 despite significant industrial action.

Similarly, the accounts do not provide information on the overall rate of casualisation, but UCU research has previously demonstrated that 70% of all staff at UoB are on some form of precarious contract, while information obtained by the branch shows that there are approximately 2,500 staff on fixed term contracts with between 1,200 and 1,500 of these staff being issued with dismissal notices each year. Meanwhile, at the top of the organisation, due to new appointments average University Executive Board (UEB) pay has dropped slightly but remains at over £200,000 pa per executive, with the Vice Chancellor, David Eastwood’s, pay once again rising, bringing his total remuneration to £450,000 pa. The figure for the VC did not include a performance related bonus of up to £80,000 (approved when the Vice Chancellor also chair the remuneration committee) which conveniently became payable on or after the 1 August 2019, the day after the 2018/19 financial year end. The figure also does not include his £90,000 salary for chairing the USS scheme nationally or his directorship in the private student recruitment company INTO University Partnerships Ltd.

In a nut shell

Ignore the misleading and questionable bottom line ‘deficit’ – the University remains in a strong cash rich financial position, albeit with a significantly more risky ‘business model’ going forward that has become structurally reliant on casualisation, international tuition fee income, and debt. There continues to be one rule for those at the very top and another for the vast majority of staff who deliver value for the University every day. The University continues to find hundreds of millions of pounds for physical assets, executive and senior faculty pay, and their new campus in Dubai, while citing uncertainties in the market when it comes to precarious employment, below inflation pay rises, and refusal to invest in student services (such as mental health services) or staff services (such as subsidised childcare).

James Brackley, Lecturer in Accounting at the University of Birmingham Business School

This article builds and draws on the recent USS Briefs article: Autocratic leadership and cowboy management: the case of David Eastwood and the ‘post’ neoliberal university

Notes:

[1] This is per hour of the taught progamme assuming 3 contact hours per week per 10 Cr and assuming all or most of the cohort is overseas students. It is an upper end estimate of the potential income per hour, but there are many such courses across several Colleges.

[2] This figure will vary depending on practice but this calculation assumes a mid-range estimate based on one hour prep time for one hour delivery for class sizes of 30 students. The cost is doubled to include admin time assuming delivery by a two legged member of teaching staff. The calculation would be considerably more complex for a three legged member of staff as we would also have to estimate research income, but based on the overall numbers in the accounts the marginal profit per hour for the University will typically be lower for three legged staff due to cross subsidisation. This argument was initially used in the College of Arts and Law for cutting research allowances for three legged staff to 25% before BUCU intervened.

[3] Estimate based on taking the mid-point for each salary range in the disclosure in note 7. multiplied by the number of staff in each category.

[4] This is based on estimates of the number of support staff in each salary category and how they will be affected by the 2019/20 support staff pay offer.

Leave a comment