The University of Birmingham has recently released their latest set of accounts (pdf), along with institutions across the sector, in which an artificial deficit of £115.4m has raised serious questions about manipulation of the accounts across the sector as negotiations with UCU over pay and pensions are ongoing.

Nationally, USS institutions across the sector have posted estimated ‘pensions provision(s)’ coming to tens or even hundreds of millions of pounds in light of the flawed 2017 valuation. The University of Birmingham has posted a £126.7m provision in generating a £115.4m annual deficit, one of the largest in the sector, while King’s College London posted the largest such adjustment so far coming to £166.7m in generating an overall deficit of £154.3m. The University of Birmingham’s accounts raise a number of other concerns too – they appear to have failed to disclose the staff numbers for staff at the new Edgbaston Park Hotel, which ran its first year of trading from July 2018 employing over 100 staff on significantly reduced pay and conditions, and they have failed to disclose the extent of our financial commitment to our new Dubai campus

[Update: in a response to BUCU the University have confirmed that there was in fact a minor error in note 7. to the accounts so that the total number of staff on page 57 should be 7,773 (rather than 7,575) to include 103 staff at the new Edgbaston Hotel and 95 staff at the University of Birmingham school. The University have also confirmed that the new note 20. on page 69 on future lease commitments does in fact relate to the Dubai campus so that the total contract value comes to £101.0m (£99.4m future commitments plus £1.6m in year cost). This corresponds to the £100m figure previously reported by BUCU.]

Pensions controversy – the wrong accounting treatment, done badly?

The Times Higher Education recently reported a long list of USS institutions disclosing huge one-off pension costs, almost all of which led to large annual deficits in their accounts. The University of Birmingham’s Treasurer’s report states that this was a result of the large deficit in the USS nationally:

“The USS scheme provides defined benefits for members and the University contributes through a scheme-wide contribution rate. This means the University is exposed to the shared actuarial risks and needs to recognise a liability for its contribution to the deficit recovery plan” (University of Birmingham Annual Accounts, 2019, pg.8)

The Treasurer’s report goes on to state that there is a “long-term challenge to the fund” and that there is “considerable risk to [its] long-term financial sustainability unless appropriate action is taken”. After a lengthy preamble about the unaffordability of the scheme there is one disclaimer sentence at the end of the report pointing out that much of this will “reverse” in 2019/20. This is in fact because, in September 2019, details of the updated March 2018 valuation that replaced the widely discredited 2017 valuation were made available to employers. As followers of the USS dispute will know, it was the 2017 valuation that formed the basis of employers’ proposals to dismantle the defined benefit elements of the scheme and to propose the transfer of risk from employers to employees. Buried in the University’s accounts (see pg.69, note 19) it turns out that they had in fact calculated the impact of the revised 2018 valuation on this year’s accounts – a reversal of £81.6m, to be pushed into 2019/20.

This is where the basis of the accounting treatment begins to look extremely flaky indeed. On page 38 of the University of Birmingham’s accounts, the accounting policy note justifies the treatment of the huge one-off cost in the main statement of income and expenditure as follows:

“The USS and NHSPS are a multi-employer schemes for which it is not possible to identify the assets and liabilities of each organisation due to the mutual nature of the schemes and therefore they are accounted for as a defined contribution retirement benefit schemes” (University of Birmingham Annual Accounts, pg.38)

With reference to FRS 102 this explanation suggests that the accounting treatment was due to the inability of the University to estimate the actuarial gains and losses reliably so that the scheme would instead be accounted for as a defined contribution scheme. I.e. only the costs relating to the current accounting period would be included. However, this is not how they are actually accounted for in the accounts and directly contradicts the explanation given in the Treasurer’s report, which stated that the one-off cost was precisely due to the exposure to such actuarial risk over the life of the scheme. The accounting policy also seems to be contradicted by the estimate of provision itself, which, in note 18. is described as follows:

“In calculating this provision, management have estimated future staff levels within the USS scheme for the duration of the contractual obligation and salary inflation”

Similarly, note 26. suggests the provision has been calculated based on the overall outstanding assets and liabilities of the scheme. This is not normally correct under defined contribution accounting under which only the costs associated to the current account year should be included, and provided for only to the extent that payments in the current accounting period were exceeded by the likely liability relating to services rendered in the current accounting period.

Instead of accounting for the current year cost, however, The University of Birmingham and other institutions have instead accounted for the present value of the artificial deficit on the scheme based on all future deficit contributions of 5% from April 2020. This is technically allowable if they could genuinely not estimate their share of the scheme assets and liabilities. However, in reality, they are effectively accounting for the scheme as a defined benefit scheme in recognising their exposure to the artificial deficit, while accounting for the scheme as a defined contribution scheme in order to bring this exposure into the income and expenditure statement so that it looks like a real cost to the institution.

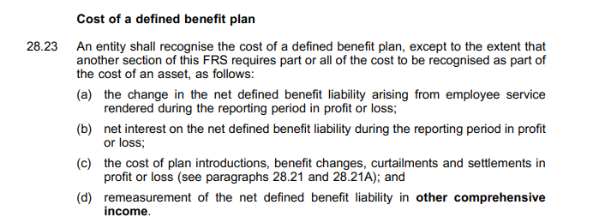

If they had just accounted for the scheme correctly to begin with, as a defined benefit scheme, it is quite clear from FRS 102 that they would not have been allowed to include the cost in this way. See FRS 102 28.23 point (d) (original emphasis):

Ordinarily, actuarial adjustments are kept separate from the main statement of income and expenditure precisely because they distort the results. They are ‘unrealised’ gains and losses and are therefore dealt with as a movement in reserves (in this case it ought to go directly to unrestricted funds). The treatment of the University’s other major scheme reflects this – see for example the £6.3m actuarial gain on the University’s own BPAS scheme (pg.45&46) is not included as regular income. So where has the advice to HE institutions to give the USS scheme special treatment come from and why are all USS institutions using the same flawed accounting? It is because it follows advice detailed in the Further and Higher Education Statement of Recommended Practice (SORP) as prepared by Universities UK. That’s the same Universities UK who sought to undermine the scheme in the first place who are now insisting upon a form of accounting that transfers the artificial deficits of their flawed valuations to the bottom line of Universities as if they were real losses!

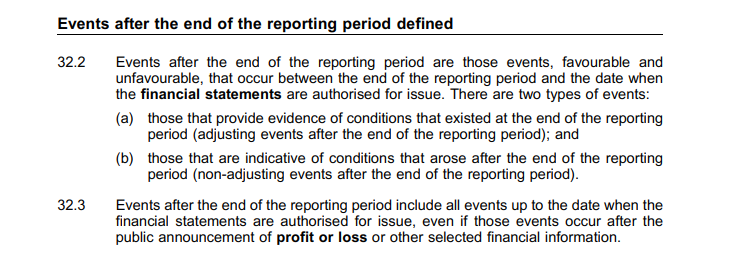

Furthermore, not only does the Universities UK accounting treatment appear to be contradictory, and potentially wrong under accounting standards, Universities do not even appear to have applied it correctly. The unassuming note 19. In the University of Birmingham’s accounts declares that the 2018 valuation reverses out £81.6m of the current year loss. This is because the 5% deficit contributions from April 2020 do not exist and the latest proposals, shared with employers in September, propose just 2% employer contributions. This has conveniently been excluded, dismissed as an “event after the reporting period” (pg.69). However, this is not correct. UK GAAP accounting proposes two potential treatments for such events depending on whether they are “adjusting” or “unadjusting” events. FRS102 describes adjusting events as events for which the conditions existed at year end but which only crystallise and become clear after year end. This would appear to be a classic example – the current obligation of the past (supposedly) pensions deficit as at 31 July 2019 was subsequently found to be £81.6m lower than the figure in the accounts due to the disclosure in September of the details of the revised 2018 valuation. Therefore, even applying the accounting treatment outlined by Universities UK under which the movements in the provision are recognised as regular expenses, the expense in the accounts should have been adjusted to reflect the 2018 valuation:

And as if all of that wasn’t bad enough, not only was the hugely material amount of £81.6m not accounted for correctly, instead being treated as a post balance sheet unadjusting event, there is no disclosure whatsoever in the audit report. The auditors of higher education institutions, in the case of the University of Birmingham this was Deloitte, have a duty not only to audit the accounts to ensure that they are true and fair and properly prepared, they also have a duty to draw users’ attention to significant disclosures of future events and material uncertainties. Despite the University of Birmingham including an expense of £126.7m that was highly subjective and incorrectly accounted for in order to mislead the users of the accounts, and incorrect by at least £81.6m even according their own estimate, nothing was included in the auditors’ report. No emphasis of matter and no modification of their opinion, despite, or perhaps because of, an audit fee for Deloitte of £172,000 (pg.58).

All of this raises serious questions for the sector, for Universities UK, and for the accounting profession charged with overseeing this process. The Financial Reporting Council (FRC) needs to get involved and investigate these practices, while audit bodies should be mandated to provide long form audit disclosure and treat HE and FE institutions as Public Interest Entities.

James Brackley, Lecturer in Accounting at the University of Birmingham Business School

[BUCU has contacted the University of Birmingham for a response to the questions raised above. The University have confirmed that they adopted the UUK recommended accounting treatment of the present value of future deficit payments under the 2017 valuation proposals. The article was amended on 23.01.2020 to clarify that the deficit was calculated based on the proposed 5% employer contributions to the deficit recovery plan, which was replaced by the 2% recovery plan following the 2018 valuation. The lower 2% recovery plan will lead to the £81.6m reverse adjustment next year.]

Leave a comment